A Personal Umbrel Lightning Node Setup

The Bitcoin Wars Part XV

Find other Bitcoin Wars articles here.

Saturday I injured my back during a workout. I've been spending my time stretching and rest. Steroid painkillers are helpful, but I likely won't do much aside from tomorrow's RTE's Roundtable discussion with Tessa Lena and Riley Waggaman for a few days. This is the first time I've been at my desk at all in 48 hours, so my wife has given me permission to release her second RTE article. Enjoy.

Introduction

I think I first heard about bitcoin at a programming meetup sometime in 2012. It tickled the part of my brain that was long ago intrigued by Scottish Free Banking and the economic thought experiment of a mud brick decentralized currency. For many years, that's mostly what bitcoin remained for me: an interesting exploration of the creation of shared value. A worthwhile experiment that I was happy to observe from a removed distance.

Things changed... slowly. I'd note when PayPal would stop certain clientele using their network, or when Cloudflare decided it would no longer protect unsavory sites from DDOS attacks, or when AWS de-hosted content deemed objectionable. Not illegal, but objectionable. Certainly, these were powerful actors in their respective markets, but they were businesses, and the fundamental moral difference between a business decision I disapprove and state oppression is, well the State, or more precisely, the force which is used to maintain it.

The pandemic has destroyed this distinction in ways I thought, if not impossible, at least improbable. The world desperately needs an economy outside and resistant to the current institutions. I do not know if bitcoin is this, but what is most important to me right now is that I signal my belief that a new way of transacting is needed. And so, I've started supporting bitcoin (and more broadly, alternate currency) in two ways: first, by exchanging some of my dollars for alternative currencies and second, by running two full bitcoin nodes.

Part I. A (short) Introduction to Currency

Fiat. If you've perused the bitcoin- and more broadly cryptocurrency- community for more than thirty seconds, you'll have seen this word. Usually used derisively to refer to any of the existing governmental currencies, and in contrast to Bitcoin or sometimes gold and silver. So, what is fiat and how do you convert fiat into Bitcoin (and vice versa)?

Fait acompli

Fiat just means "by decree", and so a fiat currency is a currency which exists not because it has intrinsic value, but because it was decreed into being. The dollars in my pocket are intrinsically worth very little. A bit of paper and ink, with minimal artistic or practical value. Their true value is derived from the governmental decree that they are the official currency for a military, commercial, resource, and technological powerhouse: the United States. If the US ceased to be these things, or if other countries and individuals who currently hold and transact in US denominated dollars ceased to believe that the US was these things, the US dollar would revert to being valued only as ugly wallpaper or fire kindling. Indeed, this is perhaps the most common route of fiat currencies-- when the government that decreed a currency loses power, that currency loses value.

Fiat currency stands in contrast to commodity based and commodity backed currencies. A commodity is an economic good like bushels of wheat, precious metals, or similar. In a commodity-based currency, trades are denominated in terms of the commodity. This can work well enough, in certain circumstances, but can also create problems. Your corn goes bad given sufficient time. Precious metals are heavy, and transporting large quantities is both risky and costly. In a commodity backed currency system, while you may use paper or digital money for ease of use in daily transactions, you can exchange your paper for the underlying physical commodity at a defined rate. Gold, having certain characteristics like non-perishability and relatively stable supply, was commonly used to back currencies. Indeed, US dollars were once denominated against a "gold standard". You'll note the operative word "once" here. Historically, commodity backed currencies were still generally state creations, and, therefore, liable to manipulation by the state. At their discretion, states have changed the rate at which a currency marker could redeem the underlying commodity (2 units instead of 10), changed the commodity backing the currency (silver instead of gold), or simply removed any commodity backing at all (going fiat).

Why then, do bitcoiners deride fiat? Surely a digital currency, with no commodity backing is the very definition of fiat? I mean, beanie babies are at least soft and cuddly. No one ever cuddled a bitcoin.

This brings us to the concept of "ideal money". What are the requisite characteristics of the best possible conception of money? Clearly, it needs to be transferable with minimal transaction costs. It shouldn’t be imitate-able (ie: defrauding someone with pyrite instead of gold), or at least the costs of imitation should require such a significant outlay of value that the costs of fraud are prohibitively high. And its valuation shouldn't be subject to centralized manipulation. It is not surprising that bitcoin meets many of these characteristics, because bitcoin was conceived as an experiment in creating ideal money. These are the characteristics, then, which help create the value of bitcoin. Bitcoin also incorporates a redundant, distributed ledger which is critical to the security of the asset. Everyone who mines bitcoin is also operating a full bitcoin node, which records each transaction that occurs on the Bitcoin network. Miners, therefore, are key components to the security of Bitcoin.

Part II: Getting Bitcoin

All this is well and good, but how does one actually go about getting bitcoin? Currently, there are two primary ways: mine it or buy it. A detailed discussion of mining is outside this bitcoin how-to. Suffice it to say, bitcoin is generated by spending increasing amounts of computational time and power solving complex polynomials. The cost of the first bitcoins mined was quite low, and the amount of computation power needed to solve the early polynomials was such that many early miners used common computers. Now, the computational demands are such that large numbers of specially designed computers are required to make bitcoin mining cost effective. A much simpler way to procure bitcoin, then, is simply to buy it. This has been rendered even more user friendly by the rise of several bitcoin exchanges. You can even buy bitcoin through PayPal, though their transaction fees are exorbitant.

The easiest way for most people to buy bitcoin is to go through an exchange like Coinbase, Gemini or Kraken. However, I’d recommend against using their normal consumer portals. The transaction costs to purchase bitcoin in the consumer-facing versions of these sites are quite high, and you can save significant amounts (generally upwards of 1% of the transaction value) by using the “trader” versions of each of these platforms. For Coinbase, this means you want a “Coinbase Pro” account, not a regular “Coinbase” one. For Gemini, you’ll want to enable “Active Trader” under settings. For Kraken, use the Kraken Trading Platform site. When you set up an account, do make sure to properly secure it. This means two factor authentication through something like Authy at a minimum. All the listed exchanges will also make use of a physical security key (such as a yubikey).

Once you’ve done this, you’ll fund your account through an ACH bank transfer (free or cheap), a credit/debit card (not generally free), or similar. When your funds are available, you’ll be able to buy bitcoin. The first way to buy bitcoin is to place a “limit” order, which means you set the price and amount you are willing to purchase (say you want 0.1 BTC and are willing to pay $20,000). Alternatively, you can set a “market” order. For a market order, you only set the amount you want to purchase, not the price. Your order will be filled at whatever the current market price is when bitcoin becomes available to sell to you. Most of these crypto exchanges currently seem to charge the same transaction fee for market and limit orders, but do doublecheck as the fee structures change. Market orders usually get filled quickly, but if bitcoin is bouncing around a lot in price, there is always some chance that you end up paying rather more (or less!) than you expected with this type of order. Limit orders generally take longer to fill (and will never fill if no one wants to sell at the price you want to buy), but you are lowering your purchase price volatility with this type of order. Do note that both limit and market orders stay “open” until they are filled or canceled by you. Also note that both limit and market orders can partially fill. For a market order, this means you may buy your total order in pieces, all of which transacted at different prices. For a limit order, this means that you may buy your order in pieces, all of which transacted at your limit price or better.

Part III: Storing Bitcoin

So that’s the abbreviated version of how to buy bitcoin. The next question is what to do with the bitcoin you bought. You can just leave it with the exchange, but there is some risk when doing this. It is always possible that a malicious actor could access your coins stored on the exchange and rob you (note that this has happened before). It’s also possible that the company itself might simply fold up shop and run away with all the stored assets (this has also happened before). Unless you have a specific reason to leave your coin on the exchange, it’s best to transfer your bitcoin to a bitcoin wallet that you control. This is a special type of storage, which records an address which contains the bitcoin as well as cryptographic keys necessary to access the Bitcoin located at that address. Wallets can be software based, hardware based, or simply a physical (or mental) record of the address and associated cryptographic keys. These latter wallets are commonly referred to as “paper wallets''. If you lose the keys, you lose your bitcoin, so the storage of the keys is of utmost importance. Software and hardware wallets store the keys for you. You access your wallet by entering a username and password, just as you would for most other applications. As this password is protecting your bitcoin, make sure it is secure and also make sure to secure your wallets with 2FA. There is some risk that a malicious software company or hacker could potentially harvest your keys (and hence your bitcoin), so you may want to keep the amounts in these types of wallets small. Hardware wallets are generally considered safer than software wallets, as the risk of hacking/harvesting is only present when the wallet is used. Software wallets are always potentially vulnerable. Breaching the security of paper wallets requires breaching the physical security of the wallet. Of course, if you lose your paper wallet, you lose your bitcoin. Always make sure your passwords (hardware/software wallet) and/or address and keys (paper wallet) are robust to the risk of loss whether through misplacing, natural disaster, robbery, etc.

If there is one thing bitcoin teaches, it is personal responsibility.

Part IV: Transacting with Bitcoin

Transacting in bitcoin involves transferring bitcoin residing at one address to another address. To receive bitcoin, the sender only needs the address at which you want to receive that coin. Note that it is considered a security risk to reuse addresses. Most software and hardware wallets automatically generate new addresses for each transaction. However, if you are receiving bitcoin into a paper wallet, best practice is to generate a new address and keys for each transaction. Always remember, the balance at a bitcoin address can be zero! It’s perfectly fine to create several empty wallets for future use. To send bitcoin, you’ll need the receivers’ address as well as the address and keys from the wallet you are using to fund the transaction. Sending is simplified if your bitcoin is stored in a hardware or software wallet, as all you need is the recipient's address and your software or hardware wallet password. To send bitcoin from a paper wallet, you’ll need to upload that paper wallet into a software or hardware wallet. You can then send any remaining bitcoin back to a new paper wallet for long term storage.

Part V: Running a Full Bitcoin Node

One important way to support bitcoin is simply to become part of the bitcoin network by purchasing and transacting in bitcoin. Just as much of the value of Twitter is due to its large user network, much of the value of bitcoin is due to its user network. The larger that network, the more valuable bitcoin becomes.

Another way to support bitcoin is to run a full bitcoin node. A full bitcoin node is part of the distributed ledger technology which underlies bitcoins value. If you choose to run a full bitcoin node, you are contributing to the redundancy and robustness of the bitcoin ledger by creating and maintaining your very own copy of all bitcoin transactions. Each bitcoin transaction is validated through at least six bitcoin nodes before being finalized, and so your node can sometimes be used not just as a passive transaction record, but also for active transaction validation.

Running a bitcoin node has been simplified of late, and initial node setup can now be completed in less than half an hour for a sub $200 investment. Running a bitcoin node is not particularly computationally intensive, and pretty much any machine made in the last 10 years can complete the task. However, because a bitcoin node is always on and always consuming energy, it is recommended that you utilize a low energy consumption device like a raspberry pi, other single board computer, or a NUC to make things as cost effective as possible. Do be aware that, unlike miners, who receive bitcoin in exchange for their computation resources, running a bitcoin node is not directly compensated.

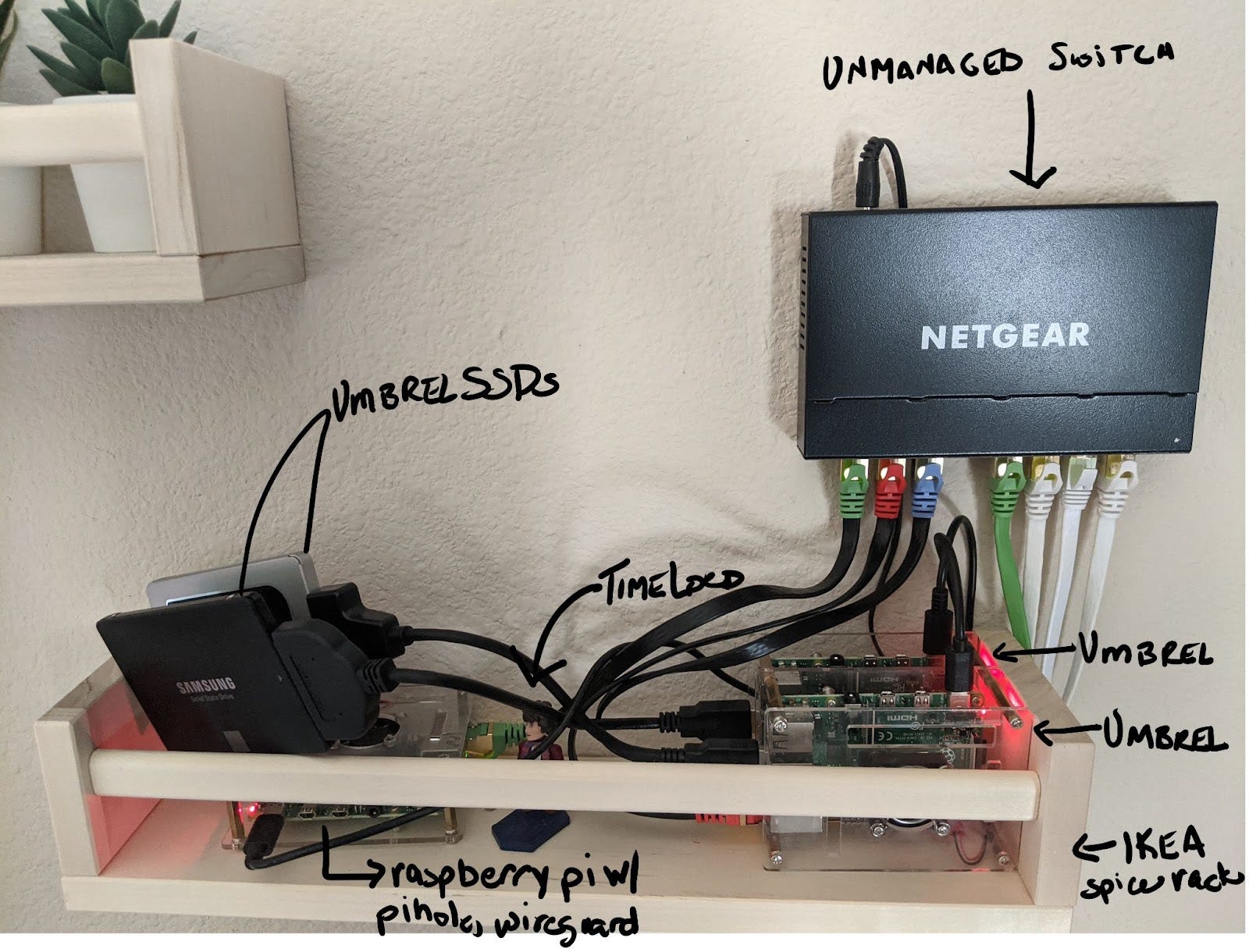

Perhaps the simplest way to set up a full bitcoin node is via Umbrel. This is an extremely user friendly setup, which utilizes a raspberry pi 4 (good luck getting one!), a16GB microSD card, a 1TB SSD, cheap case, ethernet cable, and a USB to SATA adapter. You’ll also need to download Balena Etcher and make sure you have a microSD card reader available on one of your computers. The Umbrel setup procedure is well documented at the Umbrel site. Once you’ve completed the initial setup, it’ll take several days for your new bitcoin node to fully sync with the bitcoin ledger. Do note that by default an Umbrel bitcoin node is not a listening bitcoin node. This is done for network security purposes (no need to open a port) and means that your bitcoin node doesn’t allow inbound connections from other nodes. Your Umbrel bitcoin node can be accessed via a web interface over the local network, via ssh, or directly by connecting a monitor and keyboard to the raspberry pi. Do note that if you use ssh, the default user is just “umbrel” and the password is the one you chose during setup. I generally use PuTTY as my ssh client, although ssh support is built into the mac terminal and windows power shell.

Here is my setup: I’m running a pair of Umbrel nodes together with a third pi running pi-hole, unbound, wireguard and a few other things.

If you do choose to keep bitcoin in a Umbrel connected wallet, always remember that the security for that bitcoin consists of 1) your network security and 2) the password used to secure the Umbrel during setup. In addition to the default configuration, there are a few things one can do to enhance the security of your Umbrel bitcoin node. First, turn on two factor authentication by logging in to your Umbrel via the web browser and checking the box for 2FA in “settings”. Second, disable wifi and bluetooth on the Umbrel raspberry pi and connect to the internet with an ethernet cable. Third, consider renaming your raspberry pi from the default “umbrel” to something else. Fourth, disabling or restricting via IP tables remote ssh access to the raspberry pi is possible, although I’ve not tried this myself as yet. Finally, you may consider using something like an edgerouter to create a separate, isolated network for your Umbrel bitcoin node. A common setup might involve one network for IoT devices like your smart TVs, and a second isolated network for personal computers and bitcoin nodes. You can put the Umbrel on its own network, but you’ll no longer be able to access it from your PC via the local network without first tinkering with your edgerouter firewall configuration.

In addition to running a bitcoin node, Umbrel also integrates with lots of other bitcoin/privacy related applications. You can integrate your node with several common Bitcoin software wallets, run a Bitcoin pay server, run a Lightning node, etc. Due to the aforementioned security vulnerabilities, I’d suggest keeping only nominal amounts of bitcoin in an Umbrel connected wallet.

It’s also important to be aware that the Umbrel raspberry pi operating system is written to the microSD card, while the bitcoin transaction ledger will be written to the external 1TB SSD. microSD cards are not particularly stable media, and power outages can easily corrupt written data. If you run a Lightning Node on your Umbrel, recovering your bitcoin in case of hardware failure is a bit of an ordeal. For this reason, I’d suggest either connecting your Umbrel raspberry pi to a backup power source like a conventional UPS or something like a very large power bank. Alternatively, the latest version of the raspberry pi OS enables you to boot from a connected USB drive instead of a microSD card. SSDs and conventional hard disks are more resistant to data corruption than a microSD card. Although, I’ve not done so myself, you could potentially enable boot from USB using raspi-config on the Umbrel raspberry pi and simply copy all the microSD card data onto a USB connected disk drive.

You certainly don’t need to use the Umbrel implementation to run a bitcoin node. If you’d prefer a more customizable install, you can install Bitcoin core and follow the instructions here to configure your very own bitcoin node.

Good intro, thanks! I've been running an Umbrel node for about 2 months and it just chugs along, no issues. You're right, it will be difficult to find a Raspberry Pi, tho'.

I'm generally very hopeful for the future of BTC. Two things trouble me--the pressure gov'ts can put on the exchanges and interfere with BTC being freely traded (imagine a gov't telling an exchange they can't do a transaction with anyone sending money to Canadian truckers or exchange that BTC for fiat money, for instance,) and gov't outright banning it. I just always think back to gold being confiscated and banned in the 30's.

This info is helping me understand a little better. Still very confused about the whole thing, very new for an old dog. One thing that bothers me somewhat is, where does the 'fiat' money go? What happens to it? Whose bank account is it in, and what do they do with it?